The optical communication industry is entering a new phase of accelerated growth, fundamentally reshaped by the rapid expansion of artificial intelligence (AI) infrastructure. What was once a telecom-driven market is now evolving into a core layer of global computing systems.

As hyperscale data centers scale to support AI workloads, optical interconnect technologies are becoming critical to enabling high-speed, high-density, and low-latency data transmission.

In recent years, the primary growth driver of optical communication has shifted from traditional telecom networks to AI data centers operated by cloud service providers such as Amazon Web Services, Google, and Meta.

Unlike conventional networks, AI clusters require significantly higher bandwidth and interconnect density. This has led to a sharp increase in demand for high-speed optical modules and advanced fiber connectivity solutions.

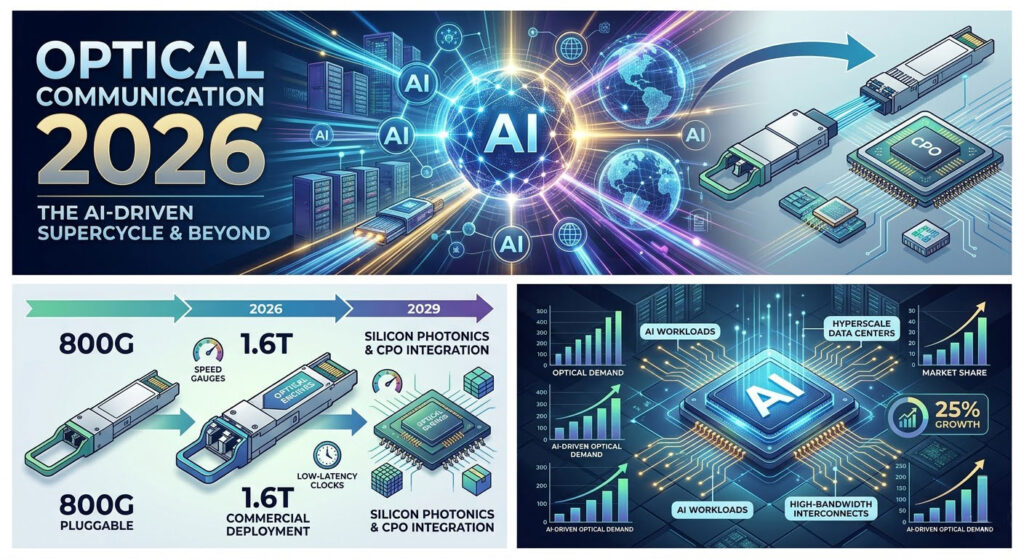

According to industry data, the global optical module market exceeded USD 23 billion in 2025 (Source: STCN), and is expected to maintain a strong growth trajectory with an estimated 25% year-on-year increase in 2026 (Source: FXBaogao). In some segments, demand has outpaced supply by as much as 2:1, reflecting ongoing supply chain constraints (Source: FXBaogao).

This demand is further amplified by AI infrastructure investments. Reports indicate that AI servers account for approximately 89% of total AI infrastructure spending (Source: EET-China), reinforcing the importance of high-performance optical interconnects.

The industry is currently undergoing a rapid transition in transmission speeds:

This upgrade cycle is driven by the exponential growth of AI workloads, where data transfer between GPUs and servers must keep pace with increasing computational power.

Over the next few months, 1.6T is expected to move from early adoption to broader commercialization, particularly among hyperscale data centers. Vendors capable of delivering stable, high-volume production will gain a significant competitive advantage.

Despite strong demand, the optical communication supply chain continues to face bottlenecks, particularly in:

These constraints are accelerating a shift toward vertical integration. Companies that control key technologies across the value chain are better positioned to ensure supply stability and maintain margins, while pure assembly players may face increasing cost pressure.

Beyond incremental speed upgrades, the industry is entering a phase of technological diversification.

Key innovation directions include:

Silicon photonics, in particular, is gaining momentum due to its advantages in scalability, integration, and cost efficiency. Market forecasts suggest that the silicon photonics segment could reach USD 10 billion by 2029 (Source: Eastmoney Research).

Meanwhile, CPO and OCS represent potential architectural shifts, moving optical connectivity closer to computing units and enabling more efficient system-level designs.

Another major trend is the evolution from component-based offerings to system-level solutions.

Instead of focusing solely on optical modules, the market is increasingly demanding:

This shift reflects the growing complexity of data center environments, where performance, scalability, and manageability must be addressed holistically.

In the short term, the optical communication industry is expected to maintain strong momentum through 2026, driven by:

Looking ahead to the next three years, several structural trends are likely to define the industry:

At the same time, global supply chains are being reshaped, with increasing emphasis on resilience and regional diversification.

The optical communication industry is no longer just a supporting layer for telecom networks. It has become a foundational component of AI infrastructure.

As AI continues to scale, demand for high-speed optical connectivity will grow not linearly, but exponentially. This marks the beginning of a new supercycle, where performance, density, and integration define competitiveness.

For companies across the optical ecosystem, the opportunity lies not only in delivering faster components, but in enabling the next generation of data center architectures.